Prepared by Tara and Kara

At BAD BEAT Investing we put out on average one high convicton, high likelihood of success idea a week. We also offer income and conviction dividend ideas monthly, have a bustling chat room of members bouncing ideas off one another, and provide a very popular thoughts on the market weekend piece. All of that for less than a cup of coffee a day! On April 1st prices to rise, so you have one week left to lock in legacy pricing. Don’t like it? There is a money back guarantee. So, if you like our thought process here, we invite you to join. Below is our just released idea for members only yesterday. Sable Offshore (SOC) stock will surge on Iran War and President Trump.

Get started today (click here)

The global energy landscape has shifted so violently in the first few months of 2026 that investors are having to rewrite their playbooks on a weekly basis. What started as a series of localized tensions in the Middle East has spiraled into a full-blown supply crisis that has sent shockwaves through the Brent and WTI markets. We have a habit of finding good opportunities, like in this financial name recently.

When we saw crude prices screaming toward $120 a barrel before finally taking a breath in the $95 to $105 range, it became clear that the era of complacent energy pricing was officially over, at least for now. For those of us watching the domestic production space, this volatility has created a fascinating and high-stakes environment where stranded assets are suddenly being viewed as national security priorities.

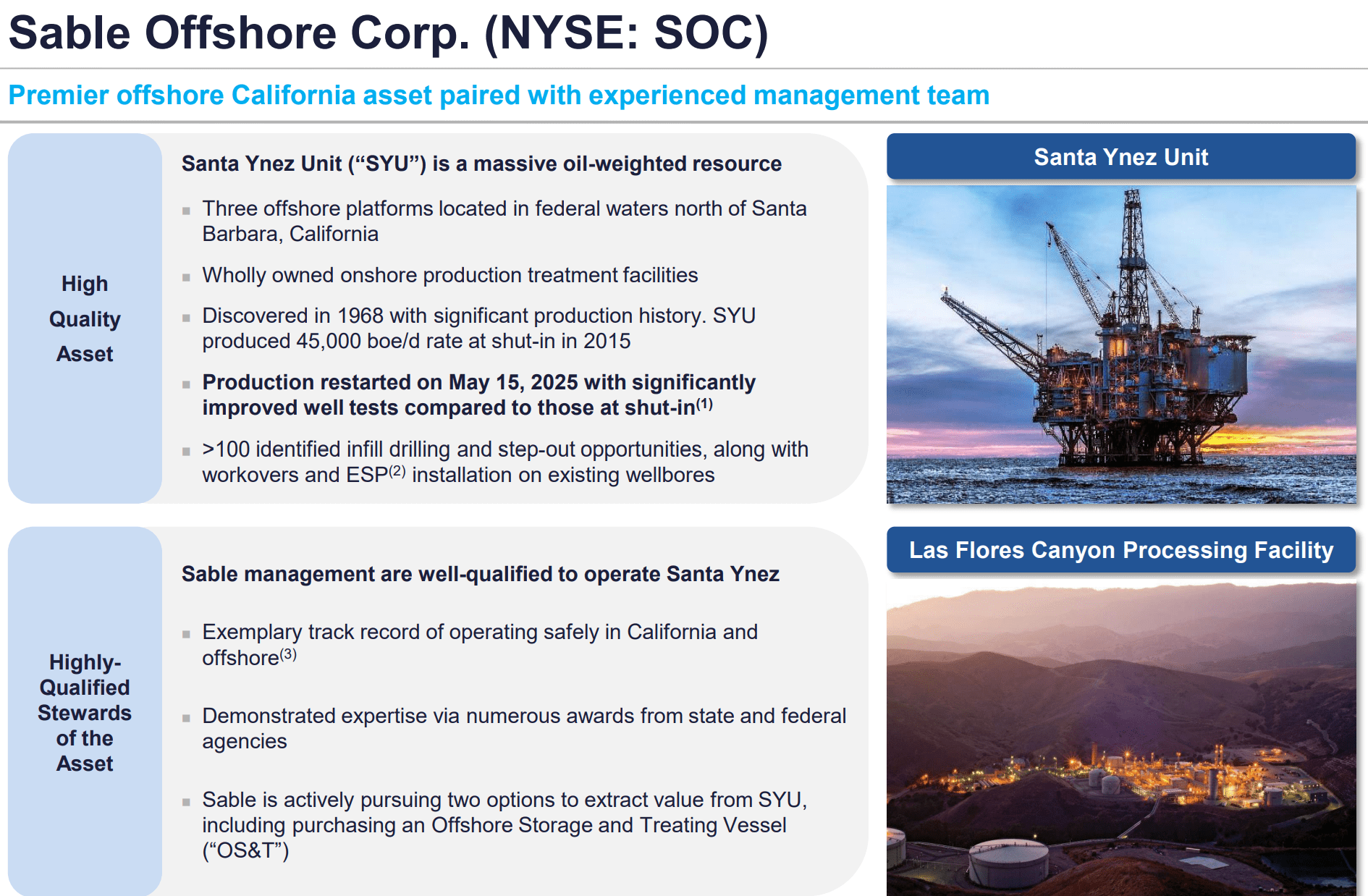

This brings us to today’s new investment, Sable Offshore (SOC), a company that has spent years navigating the dense thicket of California’s regulatory environment and local opposition, only to find itself at the center of a federal push to stabilize the global oil economy.

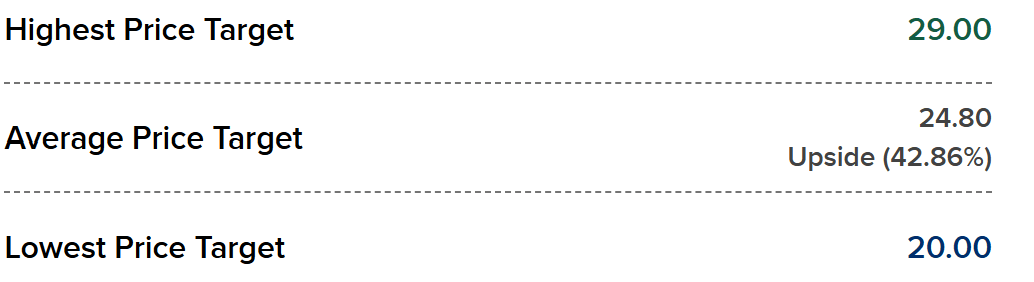

The situation in the Middle East has created a bottleneck that is hard to overstate. With the Strait of Hormuz currently acting as a primary point of friction, we are looking at a potential disruption to roughly 20 million barrels of oil per day, which accounts for about 20% of global consumption. When you add the fact that QatarEnergy has halted LNG output, stripping another 20% of the global LNG export market from the equation, you begin to see why international gas benchmarks in the UK and Netherlands have returned to the harrowing highs we saw at the start of 2025. Here the stock in question has had a bit of a run up, but we like that every major analyst covering this has a $20+ price target.

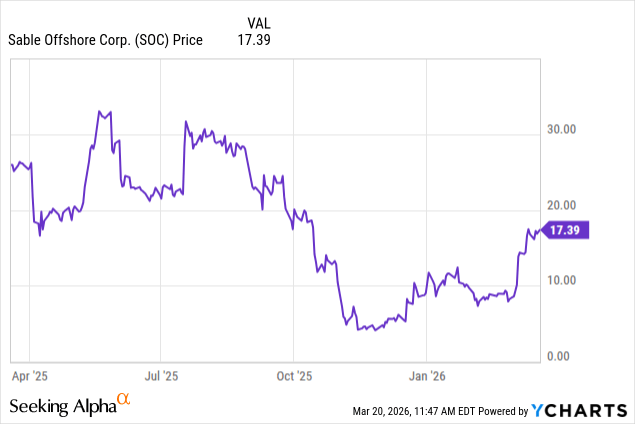

Take a look at the chart, yes, a big move was made, but there is no reason to suspect that this ends, unless we get a drastic overnight shift in the war. Unlikely, but a risk to note.

There is a bit of a cup and handle type formation here, but the draw for us is that the company is projected to triple earnings in 2027. And that assumes a more normal price of energy.

The suggested play

Target entry 1: $16.15-$16.40 (50% of position)

Target entry 2: $15.50-$15.75 (50% of position)

Suggested stop: $13.15

Target exits: $21.80 if one leg, $20.75 if 2 legs

Option considerations: We prefer commons here because bid asks are a bit wide but if you place an order in the middle of the range you can consider call options going out 7 months at the $18.00 strike for about $5. Still that is a lot to pay. Options are up due to beta. So selling PUTS is the better play here. You can sell 3/27 expiration $16 strike or $15 strike for about $0.50 or $0.30 credit respectively. Not bad for a week. Good cost basis if assigned.

Discussion

While the United States has remained somewhat insulated from the worst of the gas price spikes thanks to our local abundance, the oil market is a different beast entirely. It is a global commodity, and the urgency to find new, reliable domestic barrels has reached a fever pitch in Washington. You should be aware that in response to this, the International Energy Agency and its 32 member countries have attempted to cool the market by agreeing to release 400 million barrels from their collective strategic petroleum reserves. The United States is taking the lead here, targeting a release of 172 million barrels.

On paper, that sounds like a massive number, but when you do the math, the reality is much less comforting. This initiative is only expected to offset about 15 million barrels per day of net supply loss. Even if the global community managed to push that to 20 million barrels per day, we are talking about a 20-day supply bridge. It is a band-aid on a gunshot wound, a short-term fix that does very little to address the structural deficit created by the ongoing conflict. This is why the federal government is looking past the reserves and toward actual production growth.

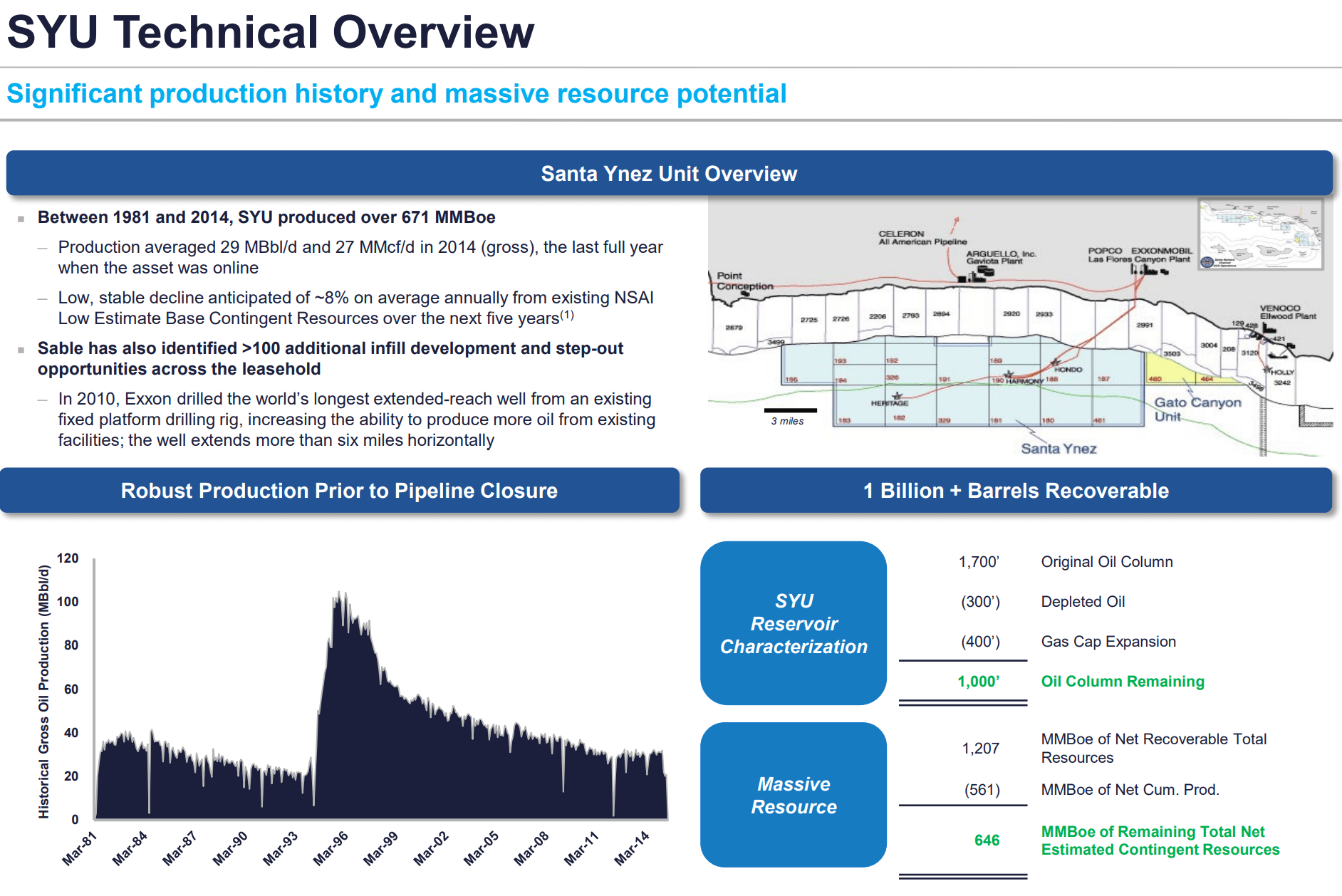

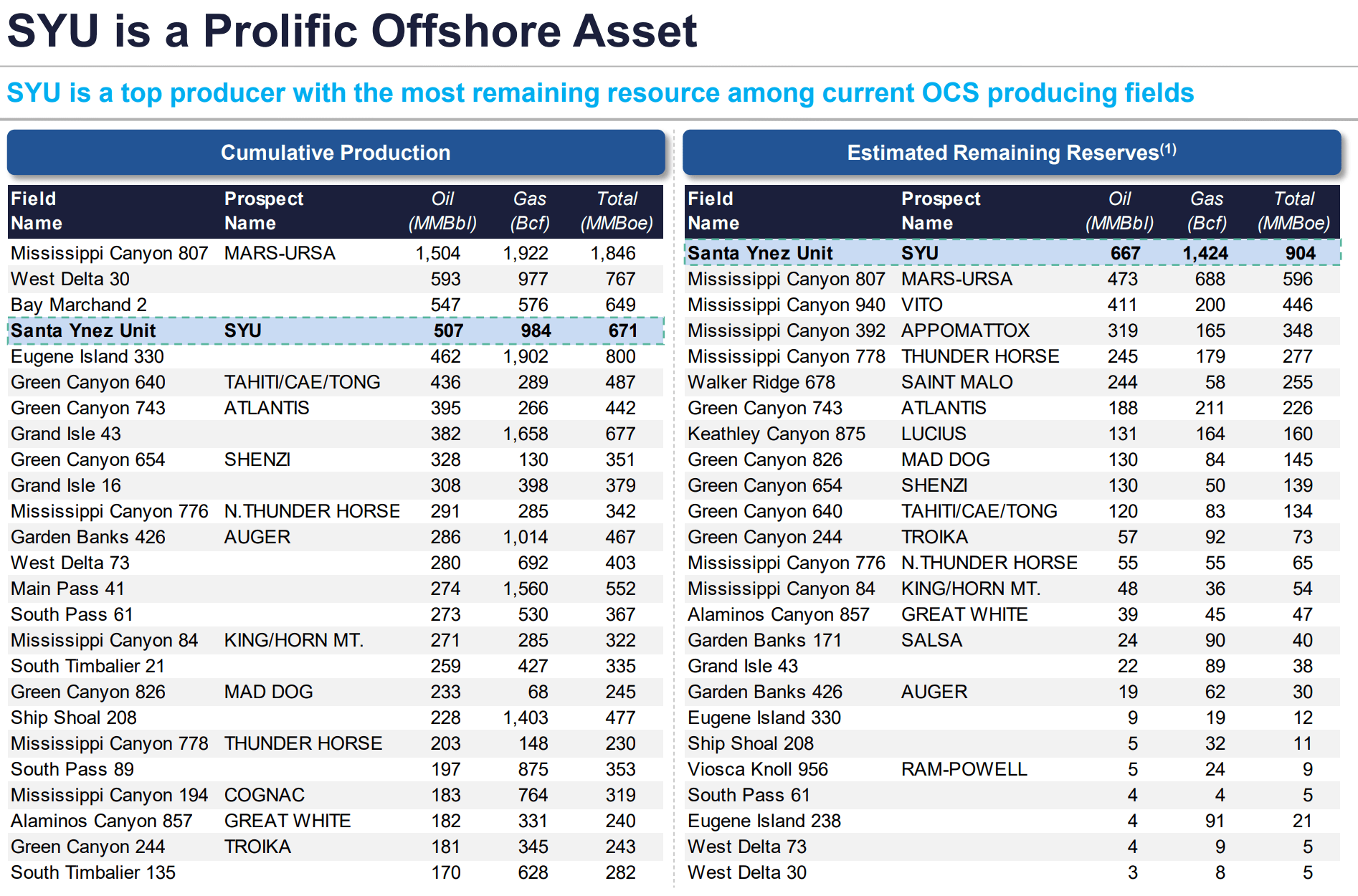

Why is the stock rallying? On March 13, 2026, the landscape for Sable Offshore changed overnight. The Trump Administration, utilizing authorities under the Defense Production Act, moved to approve the resumption of production at the Santa Ynez Unit. This is a project that has been essentially held hostage by local politics and legal challenges for years. The Santa Ynez Unit is not just another offshore rig, it is a major Pacific asset with the potential to produce roughly 60,000 barrels of oil equivalent per day once it is fully ramped up.

For a company like Sable, which has been fighting an uphill battle against the State of California and various local agencies, having the weight of the federal government behind them is the ultimate game-changer. The use of the Defense Production Act signifies that the administration no longer views this as a private commercial dispute but as a matter of urgent national interest.

The logic behind the federal intervention is grounded in the need for short-cycle flexibility and reliable domestic output. While the administration has also issued strategic waivers for Russian oil currently stranded at sea to help ease immediate pressure, everyone knows that is a temporary solution that doesn’t align with the long-term goal of maintaining economic pressure on Moscow. But we see Sable Offshore Stock to Surge On Iran War and President Trump.

Instead, the focus has shifted toward domestic development. While shale production in regions managed by companies like Exxon Mobil provides a certain level of flexibility due to its sharp decline curves and quick-to-market nature, the scale of the Santa Ynez Unit offers a different kind of prize. If Sable can get this unit back online, it represents a consistent, high-volume flow of oil and gas that can be directed either into the local California refining market or toward the hungry Asian markets across the Pacific.

From a strategic standpoint, the Pacific Coast is an incredibly valuable piece of real estate for energy production. Gas produced by Sable could be liquified and shipped to Asia, where the premium for natural gas is significantly higher than what we see in the domestic US market. However, the current “war footing” of the energy economy might flip the script. While the financial incentives for international export are compelling, the reality of high local fuel prices in California might force a preference for domestic refining. If the Santa Ynez Pipeline System is restarted, it could provide a direct line to local refineries, helping to alleviate some of the economic pressure on the West Coast. Sable currently finds itself weighing these two options: the direct export via an offshore storage and treating vessel or the traditional pipeline restart.

If we look at the numbers, the case for Sable becomes even more interesting. At full stream, we are looking at that 60,000 boe/d figure. Historically, this unit has a production mix that is roughly 86.5% oil, which means Sable could be contributing about 52,000 barrels of actual oil per day to the market. Now, skeptics will rightly point out that 52,000 barrels a day is a drop in the bucket compared to the 20 million barrels stranded in the Middle East. That is true, but in an environment where every barrel counts and the SPR is being depleted, a new source of 52,000 barrels a day that isn’t subject to Middle Eastern geopolitics is worth its weight in gold. It is about the marginal barrel and the signal it sends to the market that the US is capable of unlocking its own resources despite local regulatory hurdles.

The timeline for this production is also critical. Sable can essentially spin up production using the Las Flores Canyon and Pipeline System almost as soon as the ink is dry on the final federal approvals. If they choose the offshore storage and treating vessel route, which many believe is the more financially lucrative path, they are looking at a first sale by the fourth quarter of 2026. This puts Sable in a unique position where they are not just a story for the distant future, they are a 2026 production story. For investors, this timing is everything. It bridges the gap between the current high-price environment and the long-term structural needs of the market.

Given this backdrop, the valuation for Sable Offshore needs a serious second look. With the federal government now actively clearing the path for the Santa Ynez Unit, the risk profile of the company has fundamentally shifted. We are moving from a “will they ever produce?” narrative to a “how fast can they ramp?” narrative. Our price target of about $21 per share reflects this new reality. When you consider that SOC shares have been depressed for years due to the perceived impossibility of overcoming California’s legal barriers, the sudden removal of those barriers via the Defense Production Act suggests a massive re-rating is in order. It is a classic buy scenario where the macro tailwinds and the micro regulatory breakthroughs have converged at exactly the same time. We see Sable Offshore Stock to Surge On Iran War and President Trump.

It is also worth noting the broader political strategy at play. The administration’s move to support Sable is part of a larger push to bring creativity back to domestic production. By focusing on offshore assets that have already been discovered and partially developed, the government is looking for the fastest path to new barrels. They know that the Iranian conflict and the wider Middle Eastern instability may not be a permanent state of affairs, but the vulnerability it has exposed in the global supply chain is a lesson that won’t be forgotten.

Supporting a producer like Sable provides a strategic hedge. It ensures that even if global prices settle back down, the infrastructure for domestic independence is strengthened. For Sable, this is the moment they have been preparing for, and for the market, it is an opportunity to get exposure to a high-margin, high-growth oil play that was essentially left for dead just twelve months ago.

There are risks. First, this is a heavily shorted stock, but it looks like there has been some covering and this is likely to continue. However, it can mean there will be a lot of beta near-term. Second, California could try and do whatever it can to intervene, but they will have a hard time. Still, investing in Sable Offshore involves navigating a minefield of local opposition that might not simply vanish despite the federal government’s recent use of the Defense Production Act. While the current administration has cleared a path, the State of California and local Santa Barbara authorities have a long history of aggressive litigation that could result in eleventh-hour injunctions or new environmental challenges designed to stall the 2026 restart.

Third, beyond the courtroom, there is the massive physical hurdle of reviving infrastructure that has sat dormant for years, where any mechanical failure or unforeseen integrity issue in the aging pipeline system could lead to expensive repairs or further regulatory scrutiny. Fourth, market volatility also remains a persistent threat, as any sudden de-escalation in the Middle East or an unexpectedly effective global reserve release could deflate the triple-digit oil prices currently buoying the stock’s valuation. Finally the company’s reliance on achieving its first sale by the end of the year leaves very little margin for error, meaning any hiccup in the complex transition to an offshore storage and treating vessel could cause the market to lose patience with the timeline. Please keep that in mind.

All risks considered, and it is risky that things could change quickly, with a clear path to production by the end of the year and a federal government that is now an active partner rather than a passive observer, the road to $20+ a share looks increasingly well-paved. Sable Offshore Stock to Surge On Iran War and President Trump. Investors who can look past the noise of the Middle East and see the tangible progress being made on the Pacific Coast will likely find that Sable is one of the most compelling energy plays out there right now.

Stop Trading Against the Market. Start Investing with the Pros.

Market volatility isn’t a threat, it’s an opportunity. While the average investor is panicking, the BAD BEAT Investing community is pinpointing entries and securing rapid returns. We give you a unique playbook that combines high-conviction rapid-return trades with deep-value dividends to secure your retirement. Get in ahead of the $200 price hike April 1st!

There is a money back guarantee if you are not satisfied (you will be). Win with ideas from a team with a proven track record. Come take the next step!